Is Life Insurance Taxable In California : California S Tax System A Primer. However, any interest you receive is taxable and you should report it as interest received. Here are some of the tax implications that come with having life insurance. $420,000 x 0.4 (40%) = $168,000 (total amount owed) Taxation on life insurance premiums. Fortunately, the death benefit isn't considered taxable income, so the full payout will go to your beneficiaries.

Here are some of the tax implications that come with having life insurance. In fact, unless prohibited to do so by law, anyone can be named as beneficiary to a life insurance policy, regardless of whether he or she has any vested interest in the insured. An insurance trust is an irrevocable trust set up with a life insurance policy as the asset, allowing the grantor to exempt assets from a taxable estate. The cash value has the potential to grow over time and accrue interest. Estate taxes are paid on life insurance, if applicable.

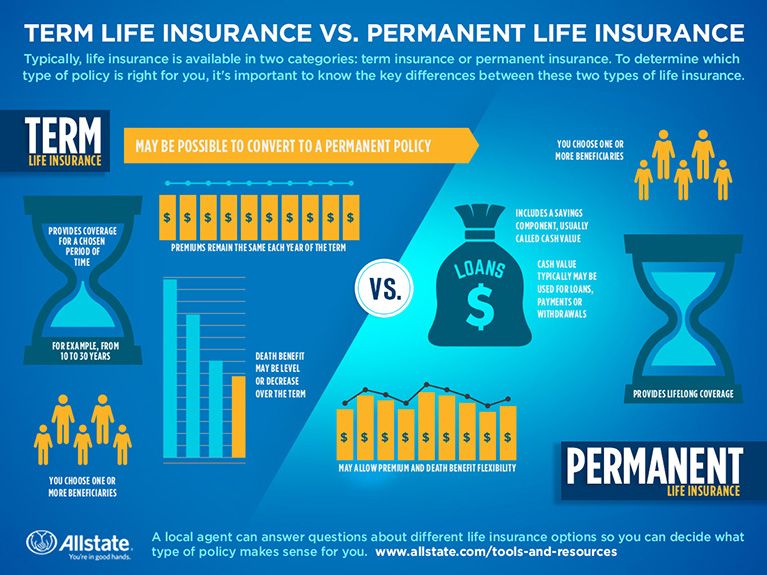

Permanent Life Insurance 101 What You Need To Know Allstate from www.allstate.com Permanent life insurance policies typically include a cash value, which can be borrowed against and potentially used to pay the premium or purchase an annuity. In this situation, the taxable amount is 40% of $420,000. Life insurance helps make sure your loved ones are taken care of in the event of your death. In general, life insurance proceeds are not taxable, but there are a few exceptions. The cash value has the potential to grow over time and accrue interest. Annual cash value growth in a life insurance policy is not usually taxable. Life insurance inside a 401k plan). Here are some of the tax implications that come with having life insurance.

Most large sums of money, like lottery winnings, are subject to tax.

Whether or not the proceeds of a life insurance policy will be taxable in the state of california will depend on how the policy was written. $420,000 x 0.4 (40%) = $168,000 (total amount owed) The cash value has the potential to grow over time and accrue interest. For the most part, the process of naming beneficiaries to a life insurance policy is the same across all states. Most commonly, the cash value of life insurance is taxable when the inheritance is a particularly large sum. Estate taxes are paid on life insurance, if applicable. Insurance companies that have received authority from the department of insurance (cdi) to transact insurance business in california are called admitted insurers and may be subject to as many as three insurance taxes in california. In this situation, the taxable amount is 40% of $420,000. He would also owe taxes on $350,000. Life insurance proceeds are not taxable with respect to income tax, so long as the proceeds are paid out entirely as a lump sum, one time, payment. Annual cash value growth in a life insurance policy is not usually taxable. There's one exception, and that's when your estate is valued at more than $11.58 million — the irs threshold for 2020. The life insurance premiums you pay are not income and therefore do not attract a sales tax.

If the beneficiary is a person, life insurance bypasses probate. Understanding taxes on life insurance premiums is also a crucial step toward finding a policy that suits your financial goals. He would also owe taxes on $350,000. Insurance companies that have received authority from the department of insurance (cdi) to transact insurance business in california are called admitted insurers and may be subject to as many as three insurance taxes in california. However, if your beneficiary receives the life insurance payment as a series of installments, the insurer will typically pay interest on the outstanding death benefit.

What Are The California Income Tax Brackets And Rates And The Amount Of The California Standard Deduction For Each Dependant Claimed Quora from qph.fs.quoracdn.net Most of the time, proceeds aren't taxable. Not subject not subject not subject • cash payments in lieu of qualified benefits. Also make sure that your life insurance company is licensed in california. Taxation on life insurance premiums. He would also owe taxes on $350,000. Life insurance proceeds are not taxable with respect to income tax, so long as the proceeds are paid out entirely as a lump sum, one time, payment. Life insurance is one of the best ways to build a financial safety net. In fact, unless prohibited to do so by law, anyone can be named as beneficiary to a life insurance policy, regardless of whether he or she has any vested interest in the insured.

Most people buy life insurance so they can leave money to their beneficiaries when they die.

But the cost (as determined by table i) of the remaining $100,000 of coverage would be. Insurance companies that have received authority from the department of insurance (cdi) to transact insurance business in california are called admitted insurers and may be subject to as many as three insurance taxes in california. For unemployment insurance (ui), employment training tax (ett), nd state disability insurance* (sdi) purposes,. There is usually no income tax paid on life insurance benefits in any state, including california. Most large sums of money, like lottery winnings, are subject to tax. In this situation, the taxable amount is 40% of $420,000. Taxation on life insurance premiums. There are some instances where the beneficiary can be taxed. The california unemployment insurance code (cuic) or by reference to the. The rate of tax on insurance varies by the type of insurance. Learn how that affects your life insurance options here.) in most cases, life insurance payouts are not taxable, which is a huge benefit. Annual cash value growth in a life insurance policy is not usually taxable. 1 however, we advise you to speak with a tax professional to ensure that all your bases are covered.

If the beneficiary takes the death benefit in installments, the interest only is taxable. But life insurance proceeds usually aren't. In addition, one of the schedules in the gross. Life insurance proceeds are not taxable with respect to income tax, so long as the proceeds are paid out entirely as a lump sum, one time, payment. This tax is paid from the estate itself, not the individuals involved.

100 000 A Year Will Make You Go Broke With The California Tax System Why California Is A Fiscal Disaster Broken Tax Structure Built On Bubbles from www.mybudget360.com The life insurance death benefit can help beneficiaries pay for college, a mortgage, and more. But there are times when money from a policy is taxable, especially if you're accessing cash value in your own policy. These services are subject to pit withholding and reportable as pit Most of the time, proceeds aren't taxable. Annual cash value growth in a life insurance policy is not usually taxable. Learn more about when taxes are due to be better prepared. However, if your beneficiary receives the life insurance payment as a series of installments, the insurer will typically pay interest on the outstanding death benefit. Not subject not subject not subject • cash payments in lieu of qualified benefits.

Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren't includable in gross income and you don't have to report them.

Permanent life insurance policies typically include a cash value, which can be borrowed against and potentially used to pay the premium or purchase an annuity. In addition, one of the schedules in the gross. There are some instances where the beneficiary can be taxed. No life insurance is not taxable in the state of california. Life insurance is designed to pay out a death benefit to your beneficiaries, if you die while the policy is in effect, usually in a lump sum. Insurance companies that have received authority from the department of insurance (cdi) to transact insurance business in california are called admitted insurers and may be subject to as many as three insurance taxes in california. However, if your beneficiary receives the life insurance payment as a series of installments, the insurer will typically pay interest on the outstanding death benefit. Any amount withdrawn above the cost basis of a life insurance policy is taxable as ordinary income. An insurance trust is an irrevocable trust set up with a life insurance policy as the asset, allowing the grantor to exempt assets from a taxable estate. Owners of annuity contracts or life insurance policies issued by companies licensed in california may be partially protected by the california life and health insurance guarantee association (clhiga) in the event of the failure of the insurer. If the beneficiary takes the death benefit in installments, the interest only is taxable. The 2017 tax law made changes to the estate tax. In most cases there is not a tax on life insurance payouts.

Is Life Insurance Taxable In California : California S Tax System A Primer. There are any Is Life Insurance Taxable In California : California S Tax System A Primer in here.