Life Insurance Proceeds Taxable To Estate / Keep Assets In Place With Insurance Premium Financing Commerce Trust Company. If the deceased person owns the policy at the time of death, then the proceeds from the policy can be subject to estate taxes. The most important factor in determining whether life insurance proceeds are subject to estate taxes is the ownership of the policy. See topic 403 for more information about interest. Incidentally, proceeds or benefits from the sss (republic act ra 1792) and gsis (ra 728) are also not subject to estate tax. Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren't includable in gross income and you don't have to report them.

When it comes to taxes, there are few simple rules. You possessed certain economic ownership rights (called incidents of ownership) in the policy at your death (or within three years of your death). For those estates that will owe taxes, whether life insurance proceeds are included as part of the taxable estate depends on the ownership of the policy at the time of the insured's death. In some cases, your life insurance proceeds can pass to. The exclusion applies to any beneficiary, whether a family member or other individual, a corporation, a partnership, or an estate.

This Is The Problem With Life Insurance As A Solution To The Estate Tax Issue Family Enterprise Usa from familyenterpriseusa.com The most important factor in determining whether life insurance proceeds are subject to estate taxes is the ownership of the policy. A second way to remove life insurance proceeds from your taxable estate is to create an irrevocable life insurance trust (ilit). For those estates that will owe taxes, whether life insurance proceeds are included as part of the taxable estate depends on the ownership of the policy at the time of the insured's death. If life insurance proceeds are payable to a religious, charitable or educational organization, is their value taxable in the insured's gross estate? Although most lumps of money, such as lottery winnings, are subject to tax, life insurance proceeds are typically not. Whether life insurance proceeds are part of the taxable estate depends on who owns the policy at the time of the insured's death. When it comes to taxes, there are few simple rules. Life insurance proceeds are typically not taxable as income, but can be taxed as part of your estate if the amount being passed to your heirs exceeds federal and state exemptions.

See topic 403 for more information about interest.

The deceased person owns the policy on the date of death. For those estates that will owe taxes, whether life insurance proceeds are included as part of the taxable estate depends on the ownership of the policy at the time of the insured's death. The tax consequences of being the beneficiary of a life insurance policy can be confusion, but this information should help. Although most lumps of money, such as lottery winnings, are subject to tax, life insurance proceeds are typically not. If life insurance proceeds are payable to a religious, charitable or educational organization, is their value taxable in the insured's gross estate? Life insurance is a fantastic way of establishing a financial safety net for your dependents. While life insurance is important and useful for many purposes, does it provide a resource to pay the estate tax for most families? You possessed certain economic ownership rights (called incidents of ownership) in the policy at your death (or within three years of your death). An irrevocable life insurance trust (ilit) is another effective vehicle that can be set up to keep life insurance proceeds from being taxed in the insured. This includes group term life insurance provided by an employer. While life insurance planning is a commonly used estate planning tool, there are several commonly held misconceptions about the tax treatment of life insurance proceeds. If the deceased person owns the policy at the time of death, then the proceeds from the policy can be subject to estate taxes. The 2017 tax law made changes to the estate tax.

See topic 403 for more information about interest. Death benefits aren't normally subject to income tax, but they can add to the value of the decedent's estate and become subject to the federal estate tax. Life insurance ownership to remove estate tax burden. Life insurance can be an effective part of estate planning, and can provide a significant benefit to a decedent's surviving family members. Although most lumps of money, such as lottery winnings, are subject to tax, life insurance proceeds are typically not.

Ian Filippini The Role Of Life Insurance In An Estate Plan from image.slidesharecdn.com That would occur if certain rules weren't met, and the overall value of the estate exceeds the annual federal estate tax exemption, which is $11.7 million. This includes group term life insurance provided by an employer. Your estate is the beneficiary of the insurance proceeds, or. Incidentally, proceeds or benefits from the sss (republic act ra 1792) and gsis (ra 728) are also not subject to estate tax. In this situation, the entire insurance payout is typically included in the estate and can be subject to estate taxes. You should make sure your life insurance policy won't have an impact on your estate's tax liability. A second way to remove life insurance proceeds from your taxable estate is to create an irrevocable life insurance trust (ilit). Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren't includable in gross income and you don't have to report them.

You should make sure your life insurance policy won't have an impact on your estate's tax liability.

If you want to preserve your legacy, the owner and beneficiary of the proceeds from your life insurance policy must be another person or legal entity. But if a beneficiary was not named, or is already. And if the payout pushes your estate past federal or state estate tax exclusion limits. The deceased person owns the policy on the date of death. Under the estate tax rules, insurance on your life will be included in your taxable estate if: Whether life insurance will be subject to the federal estate tax is generally controlled by section 2042 of the 1986 internal revenue code, which has two subsections: An irrevocable life insurance trust (ilit) is another effective vehicle that can be set up to keep life insurance proceeds from being taxed in the insured. The exclusion applies to any beneficiary, whether a family member or other individual, a corporation, a partnership, or an estate. But the benefits could be counted as part of your taxable estate. That would occur if certain rules weren't met, and the overall value of the estate exceeds the annual federal estate tax exemption, which is $11.7 million. See topic 403 for more information about interest. However, any interest you receive is taxable and you should report it as interest received. For the purposes of simplification, all assets above the estate and gift tax exemption that you own at the time of your death are subject to estate taxes.

See topic 403 for more information about interest. Using life insurance trusts to avoid taxation. An irrevocable life insurance trust (ilit) is another effective vehicle that can be set up to keep life insurance proceeds from being taxed in the insured. Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren't includable in gross income and you don't have to report them. While life insurance planning is a commonly used estate planning tool, there are several commonly held misconceptions about the tax treatment of life insurance proceeds.

Tax On Insurance Do Beneficiaries Pay Taxes On Life Insurance Aegon Lifeaegon Life Blog Read All About Insurance Investing from www.aegonlife.com See topic 403 for more information about interest. An irrevocable life insurance trust (ilit) is another effective vehicle that can be set up to keep life insurance proceeds from being taxed in the insured. Although most lumps of money, such as lottery winnings, are subject to tax, life insurance proceeds are typically not. While life insurance is important and useful for many purposes, does it provide a resource to pay the estate tax for most families? The proceeds from a decedent's life insurance policy paid by reason of his or her death generally are excluded from income. And if the payout pushes your estate past federal or state estate tax exclusion limits. Life insurance is not taxable the reality is that life insurance is treated as an asset in your estate. The life insurance payout goes into a taxable estate.

Like most assets, estate taxation of life insurance proceeds is based in part on the ownership of the life.

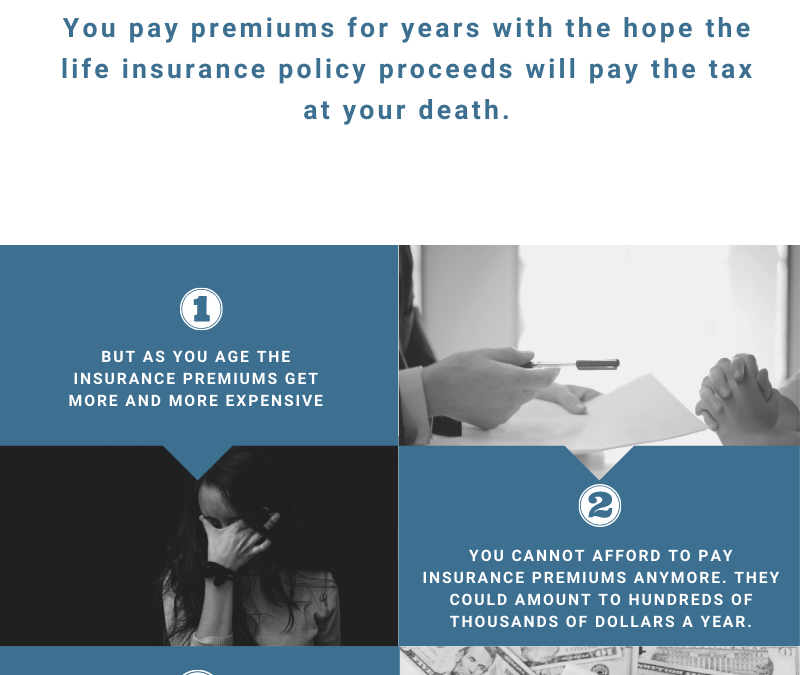

If you want to preserve your legacy, the owner and beneficiary of the proceeds from your life insurance policy must be another person or legal entity. Although most lumps of money, such as lottery winnings, are subject to tax, life insurance proceeds are typically not. The most important factor in determining whether life insurance proceeds are subject to estate taxes is the ownership of the policy. Whether life insurance proceeds are part of the taxable estate depends on who owns the policy at the time of the insured's death. If life insurance proceeds are payable to a religious, charitable or educational organization, is their value taxable in the insured's gross estate? Estate taxes only apply to wealthy estates — you can check the irs estate tax limits to see if your estate would be affected. But the benefits could be counted as part of your taxable estate. The life insurance proceeds will pass into the decedent's probate estate and become available to pay the decedent's final bills. Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren't includable in gross income and you don't have to report them. Hear one family's story in which the family member aged out of the policy and will not have the policy proceeds to pay the estate tax after decades of paying the premiums. The tax consequences of being the beneficiary of a life insurance policy can be confusion, but this information should help. Taxation of death benefits depends on many factors, as well as the nature of the taxes. Life insurance can be an effective part of estate planning, and can provide a significant benefit to a decedent's surviving family members.

0 Comments:

Post a Comment